Why Argentina might switch to the dollar

President Milei has proposed that Argentina adopt the U.S. dollar to help cure its economic woes. Politics and his own fiscal policy currently stand in the way.

In a nutshell

- Dollarization could help solve Argentina’s persistent economic woes

- Buenos Aires may opt for a dual-currency system with both the peso and U.S. dollar

- The political support and economic stability needed for dollarization are lacking

The specter of hyperinflation is looming over Argentina, and President Javier Milei is proposing dollarization as part of the solution. The process of currency substitution involves replacing the domestic currency with a foreign one – in Argentina’s case, that would be the United States dollar.

President Milei, an economics professor for over 20 years, initially leaned toward a complete dollarization plan. While that is still possible, recent developments suggest that a dual currency approach, where the peso and the U.S. dollar coexist, is more likely. Other reforms will have to be implemented as well, but dollarization is increasingly viewed as a necessary component of a new set of policy and institutional changes hoped to provide long-term solutions to Argentina’s economic woes.

The economic background for adopting a foreign currency

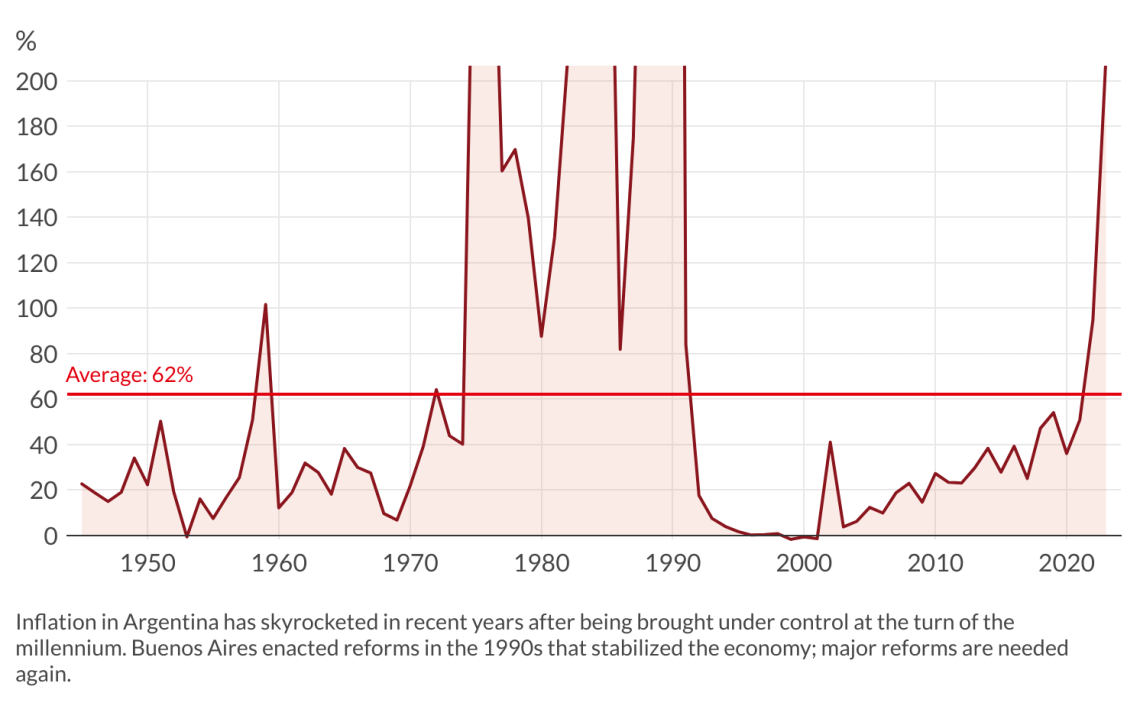

Argentina has grappled with chronic high inflation – averaging 62 percent – since 1945, except for a brief respite in the 1990s. This persistent inflation, spanning governments and political eras, points to an underlying institutional issue that requires a robust solution. The long-term consequences have included a decline in gross domestic product (GDP) per capita since the mid-1940s.

Dollarization offers a comprehensive economic reform that facilitates balancing the budget, fiscal reforms, restructuring the labor market and promoting free international trade without the potential risks stemming from domestic politics.

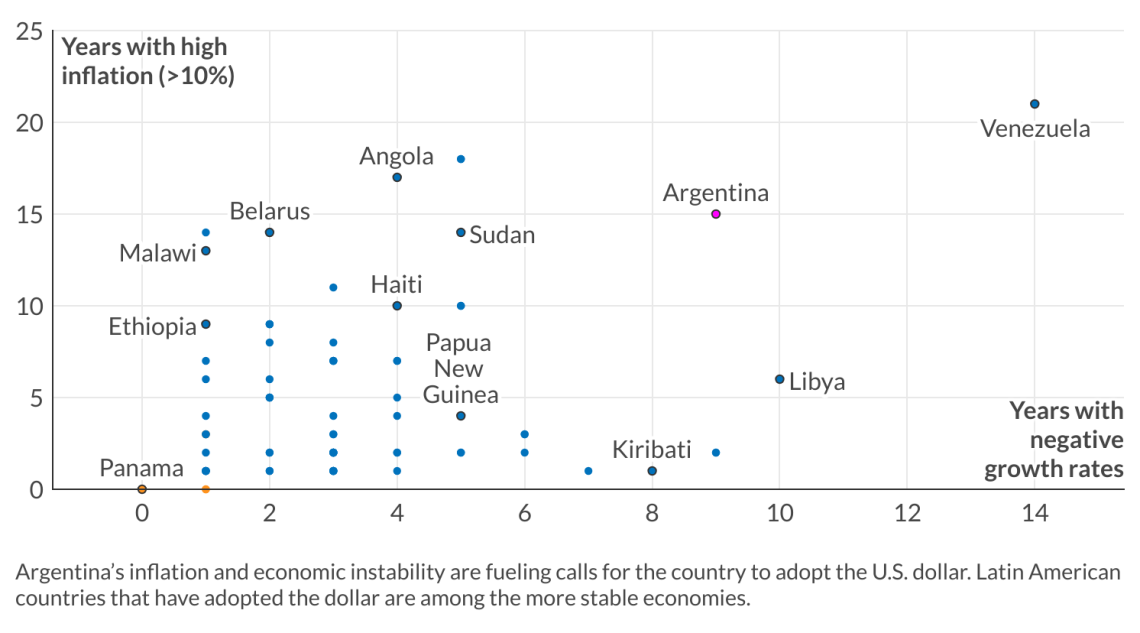

Dollarized economies like Panama, Ecuador and El Salvador have showcased resilience, stability and sustained growth, free from currency crises and bank runs. Dollarization not only mitigates exchange rate risks but also protects private sector access to credit, even during periods of government default or political upheaval, as seen in the case of Ecuador.

Political incentives in Buenos Aires

Apart from its economic advantages, dollarization offers two key political benefits for Argentina. First, it is a quick step with a rapid outcome, preserving the political capital necessary for subsequent structural changes like labor market reforms and balancing the budget. Second, dollarization can help boost output while enforcing fiscal discipline. Ecuador as well as Argentina itself during the 1990s are successful precedents for this strategy.

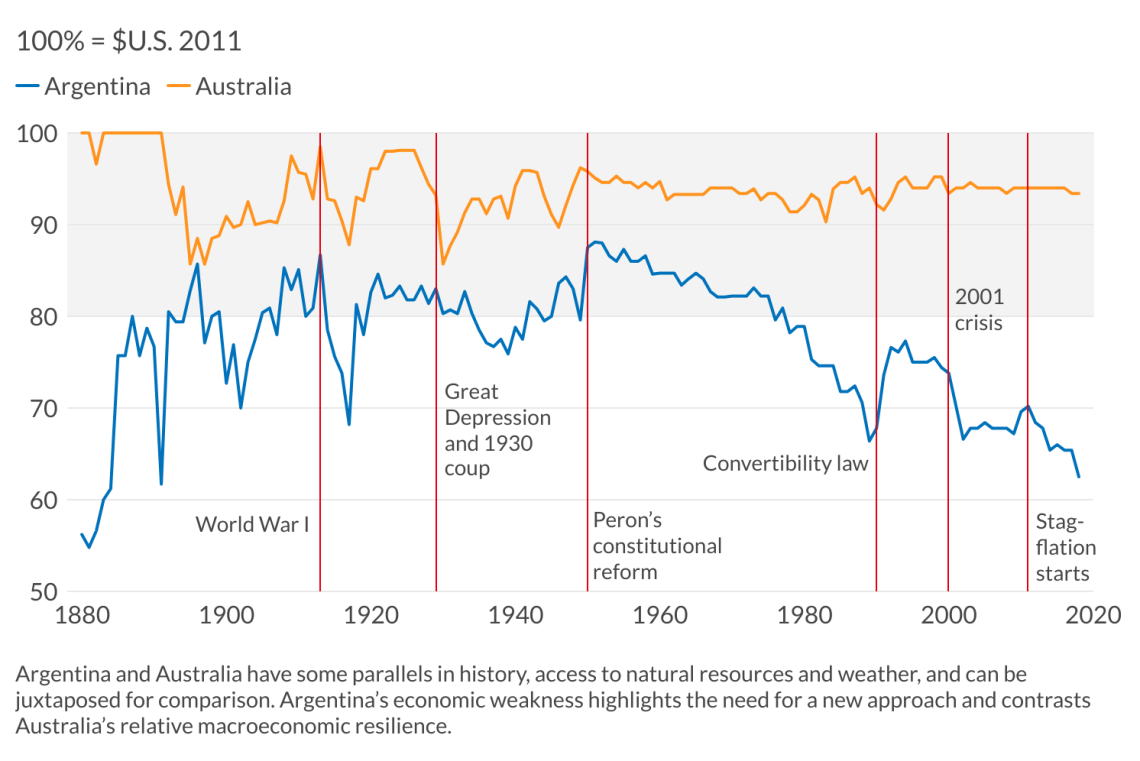

An alternative path relying on the national currency alone would take more time to offer clear economic benefits. Balancing the budget or passing regulatory reforms require debate in congress, time to implement and still more time to gauge the economic effects. Such a timeline imposes a high risk for the Argentine government under current economic conditions. Argentina shows poor macroeconomic performance at the international level, while dollarized countries in the region are among the more stable economies (see graph below).

Implementing dollarization

Implementing dollarization ideally occurs at an equilibrium exchange rate, ensuring a smooth transition without significant disruptions in economic sectors. Conceptually, it is useful to divide dollarization into three groups: bank accounts, currency in circulation and central bank liabilities.

Bank accounts represent the easiest and fastest group to dollarize. Bank deposits convert their unit of account from pesos to dollars at the dollarization rate, a process that can occur immediately as it is an accounting adjustment. In terms of physical dollars needed, in principle, only bank reserves would have to be covered.

Current conditions in Argentina make a massive bank run unlikely. Bank deposits are for transaction purposes such as goods, services, wages and other cash needs, that is, money that account owners need to have in bank accounts to make and receive payments. While the lack of low-denomination dollar bills constrains bank withdrawals, as cash transactions typically require small change available only in pesos, banks can instead offer customers debit cards loaded with dollars instead of dispensing cash. Ecuador’s experience demonstrates that a dollarization announcement, if handled right, can lead to currency returning to bank deposits despite offering a negative real interest rate.

Current conditions in Argentina make a massive bank run unlikely.

The currency that is now in circulation can be managed in various ways. One option is a mandatory dollarization of circulating currency, as seen in Ecuador, where a nine-month period allowed for the exchange of sucres for dollars before the local currency lost validity. Alternatively, voluntary dollarization, as in El Salvador, maintains the validity of the local currency indefinitely. In this case, the circulating currency is dollarized when it is deposited into banks or paid as taxes (since such funds would be entering government bank accounts).

Argentina could potentially combine both methods. Beginning with voluntary peso dollarization, after a specified period of, for example, one year, if the circulating currency falls below a predefined threshold, dollarization could automatically transition to mandatory. This approach would provide the central bank with time to acquire the necessary dollars during the voluntary period, while reducing the dollars required to only those necessary to reach and maintain the predefined threshold level.

Overcoming dollarization’s biggest challenge: Central bank liabilities

The dollarization of central bank liabilities is the most challenging aspect, as these obligations support commercial bank deposits. One option could involve the government purchasing these liabilities from commercial banks using dollars, though this would necessitate a significant dollar reserve the government currently lacks. Moreover, it would eliminate a revenue source for banks, potentially affecting them in the short term if viable alternatives are not available in the Argentine market.

Given these challenges, an alternative approach involves dollarizing these liabilities and scheduling their payment through a sinking fund, allowing repayment of liabilities through a scheduled set of payments, rather than all at once on dollarization day. This could be facilitated through an international trust, providing additional security and stability to the plan. Central bank financial assets, such as treasury bonds denominated in dollars, would transfer to the trust; central bank liabilities would be replaced with short-term, dollar-denominated liabilities issued by the trust.

Read more on challenges and potential solutions for Argentina

- Milei’s choice for Argentina: From misery to prosperity

- What does the rise of Javier Milei mean for Argentina?

- Argentina’s shaky plans to tame high inflation

The government could then initiate the central bank shutdown process, with revenue from treasury bonds and other contributions to the trust automatically applied to settle dollarized central bank liabilities. Once all liabilities are cleared, the trust would liquidate and all financial assets would revert to the government.

Importantly for the Argentine public, dollarization represents a near-immediate policy change. Once bank accounts are dollarized and the U.S. dollar gains legal-tender status, the public would operate within a “dollarized economy.” The process of exchanging pesos in circulation for U.S. dollars and addressing central bank liabilities would occur behind the scenes.

President Milei’s economic plan and options for monetary reform

While President Milei’s government has not yet disclosed a detailed economic plan and trajectory for the future, their intentions can be summarized in several key steps.

The first involves rapidly balancing the budget, followed by reducing the amount of money being printed to finance the deficit, thereby lowering inflation. There is also a plan to transfer central bank liabilities to the treasury to enhance the central bank’s balance sheet. Once these measures are implemented, capital controls will be eliminated and a dual-currency system will be established, allowing the peso and the U.S. dollar to compete on equal footing.

Furthermore, the government aims to prohibit the central bank from directly financing the treasury. Finally, once the U.S. dollar replaces the peso, the plan calls for eliminating the central bank and officially transitioning to a fully dollarized economy.

Scenarios

There are three potential economic scenarios for Argentina during Mr. Milei’s presidency, which could extend to late 2027 in a first four-year term, with full dollarization being the least likely.

Unlikely: Dollarization by conviction

Argentina would undergo dollarization as a result of a conviction-based plan, implying that it is the right decision for the country as determined by the government (this resembles El Salvador’s case). In this scenario, Argentina would experience a smooth transition to dollarization. However, there are two conditions that make this scenario unlikely: lack of time and lack of support.

Completing the full transition, including the dollarization of central bank liabilities, requires a long time, increasing the likelihood the fragile Argentine economy would face new economic or currency headwinds along the way, potentially rendering the plan impossible to fully execute. Public and political support for dollarization may diminish in this scenario as well, leading to a resurgence of calls to save the peso under the argument of “this time we can do it.”

Somewhat likely: Dollarization by necessity

Dollarization occurs out of necessity rather than conviction. This scenario unfolds as Argentina plunges into a severe economic crisis, where policymakers see no other credible reform to successfully navigate the challenges. Previous attempts at implementing measures like a currency board and popular regimes such as inflation targeting have failed. Dollarization emerges as the only robust reform left to be implemented in Argentina. If Argentina were to undergo dollarization this way, it would likely resemble Ecuador’s experience, serving as a means to avoid hyperinflation and a major financial crisis.

This scenario is somewhat likely because Mr. Milei’s current plans could precipitate such a critical situation. The government is balancing the budget primarily by reducing direct transfers to the private sector (including pensions, retirement payments and subsidies), a strategy that seems unsustainable given high poverty rates and low real-income levels. Fiscal policy itself will be insufficient to stave off crises.

A lack of credibility in fiscal policy would then undermine the disinflation process, jeopardizing the overall stability of the economic plan. In this scenario, dollarization would occur under President Milei’s government, with public support hinging on his commitment to dollarization.

Likely: The peso survives for now, with dollarization to come in a future presidency

Mr. Milei’s plan manages to steer clear of a major crisis, but he lacks sufficient political support for full dollarization. A new president could then be elected who wants to preserve the peso. A lower (though likely still high by international standards) inflation rate facilitates this course of action. However, it is important to note that this scenario does not rule out the possibility of “dollarization by necessity” at a future date, particularly after President Milei’s tenure concludes.

This scenario is likely because, for the moment, President Milei lacks a team of dollarization experts. Additionally, there is currently insufficient political support for dollarization. These points, coupled with President Milei’s antagonistic attitude toward other political parties, make it unlikely that he will be able to achieve the necessary political consensus in congress.

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.